Fed policy and the natural rate of interest—a delicate balancing act

REAL ECONOMY BLOG | May 05, 2022

Authored by RSM US LLP

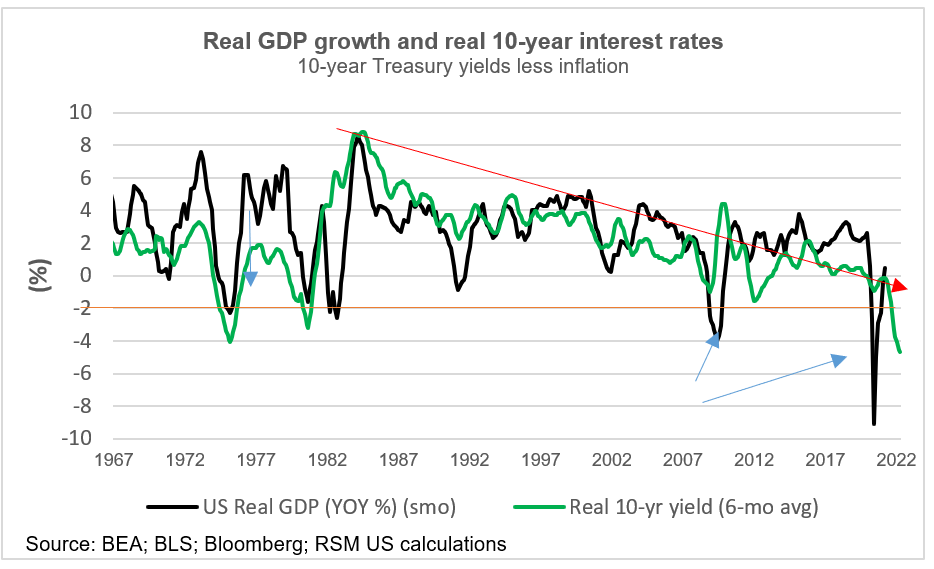

The long-run trend in U.S. economic growth has been in decline ever since the Volcker Federal Reserve put the clamps on inflation in the early 1980s, falling to below 2% per year in the pre-pandemic era.

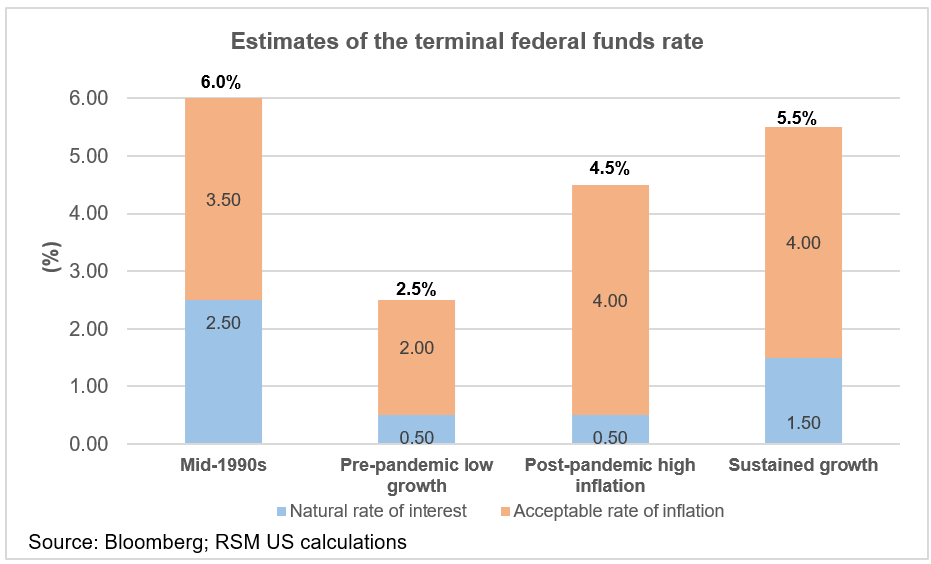

We estimate that the real natural rate of interest is 0.5%, which implies a terminal rate of 2.5%. Given the current inflation challenge, it is highly likely that the Federal Reserve will move its policy rate into restrictive terrain near 3% before the end of the year, which will cause overall economic activity to slow back toward the long-term growth trend of 1.8%.

Real interest rates (shown as the yield on 10-year Treasury bonds less the inflation rate) have been in decline as well, which is an indication of an economy no longer able to support higher rates of return on investment.

In current trading, the real 10-year interest rate is roughly negative 5%, which is indicative of the urgency at the Federal Reserve to restore price stability to the economy and move the real rate back into positive terrain.

The overriding need to raise the rate of return on long-term investments is to have an economy that can support investments in the real economy, rather than one in which the only decent rate of return is speculation in the equity market.

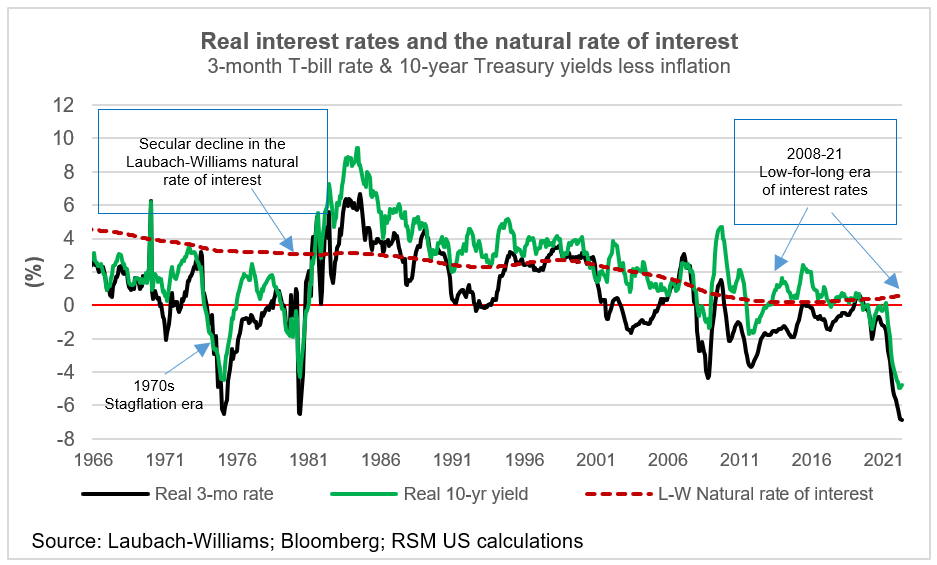

Beginning with the underlying basis of investment, estimates of the natural rate of interest—the return on investment stripping out business cycle fluctuation—have been in secular decline as well. The current estimate puts the natural rate at 0.5%, hardly enough to compensate for the risk of investment.

If one were to add expectations for inflation of 2% per year to the natural rate of 0.5%, then that would line up with the Fed’s estimate of its so-called terminal federal funds rate, which is its long-range target.

But what would happen if the Fed were to consider a post-pandemic economy with continued shortages, higher inflation and the success of the fiscal initiatives and the increased productivity that has followed greater business investment?

Let’s start with the last burst of productivity in the mid-1990s, when the natural rate of interest was roughly 2.5% and inflation was averaging about 3.5%.

That would have supported a terminal federal funds rate of 6%, roughly in line with the 5.5% to 6.5% peaks in the actual funds rate over the course of the business cycle.

Going into the pandemic, real economic growth had stagnated such that the natural rate of interest dropped below 0.5% and inflation remained stuck below the Fed’s 2% target. That would have implied a terminal federal funds rate of 2.5%.

Coming out of the pandemic, the Fed was looking for inflation to remain above its 2% target, a positive sign of higher demand powering an economic recovery. Instead—and because of supply chain shortages and now the shock of war—we can assume that inflation will remain substantially above target.

If demand were to cool because of Fed policy hikes and if the economy were to slow, we might expect the Fed to accept something like a 4% inflation rate, which implies a 4.5% eventual level for the funds rate.

And if the Fed is indeed able to balance the need to reduce inflation and if the real return on investment rises to 1.5% as productivity advancements take hold, then a terminal funds rate of 5.5% might be warranted.

That would signify an economic recovery and the wider distribution of wealth and sustainable growth that the monetary and fiscal authorities are hoping to achieve.

This article was written by Joseph Brusuelas and originally appeared on 2022-05-05.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/fed-policy-and-the-natural-rate-of-interest-a-delicate-balancing-act/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Pugh CPAs is a proud member of RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Pugh CPAs can assist you, please call 865.769.0660.

Let's Talk!

Call us at 865.769.0660 or fill out the form below and we'll contact you to discuss your specific situation.